Europa: un camino cauteloso hacia la madurez de la IA

Encuesta HLB a Líderes Empresariales 2024

Los líderes empresariales europeos se mantienen resilientes en un año difícil

La inflación y los tipos de interés resultaron agotadores en 2023. Los precios de la energía también se mantuvieron altos, mientras que el crecimiento macroeconómico se desaceleró como se esperaba. Mientras las empresas miran hacia 2024, la confianza se recupera lentamente en Europa: sólo el 28% de los líderes espera un aumento en el crecimiento económico este año frente al 41% a nivel mundial.

Sin embargo, están surgiendo los primeros signos de optimismo. Cuando se les preguntó el año pasado, el 69% de los líderes empresariales europeos esperaban una disminución en el crecimiento económico global. Este año, el doble de encuestados (31%) esperan el mismo resultado. La estabilización del suministro de energía y la transición progresiva a las energías renovables, junto con un clima más moderado, mantuvieron baja la demanda de energía, fomentando en 2023 un crecimiento económico más fuerte de lo esperado. La inflación general se ha desacelerado y se prevé que caiga al 2,7% interanual a mediados de 2024. La tasa de desempleo sigue siendo relativamente baja y continúa la normalización del crecimiento salarial.

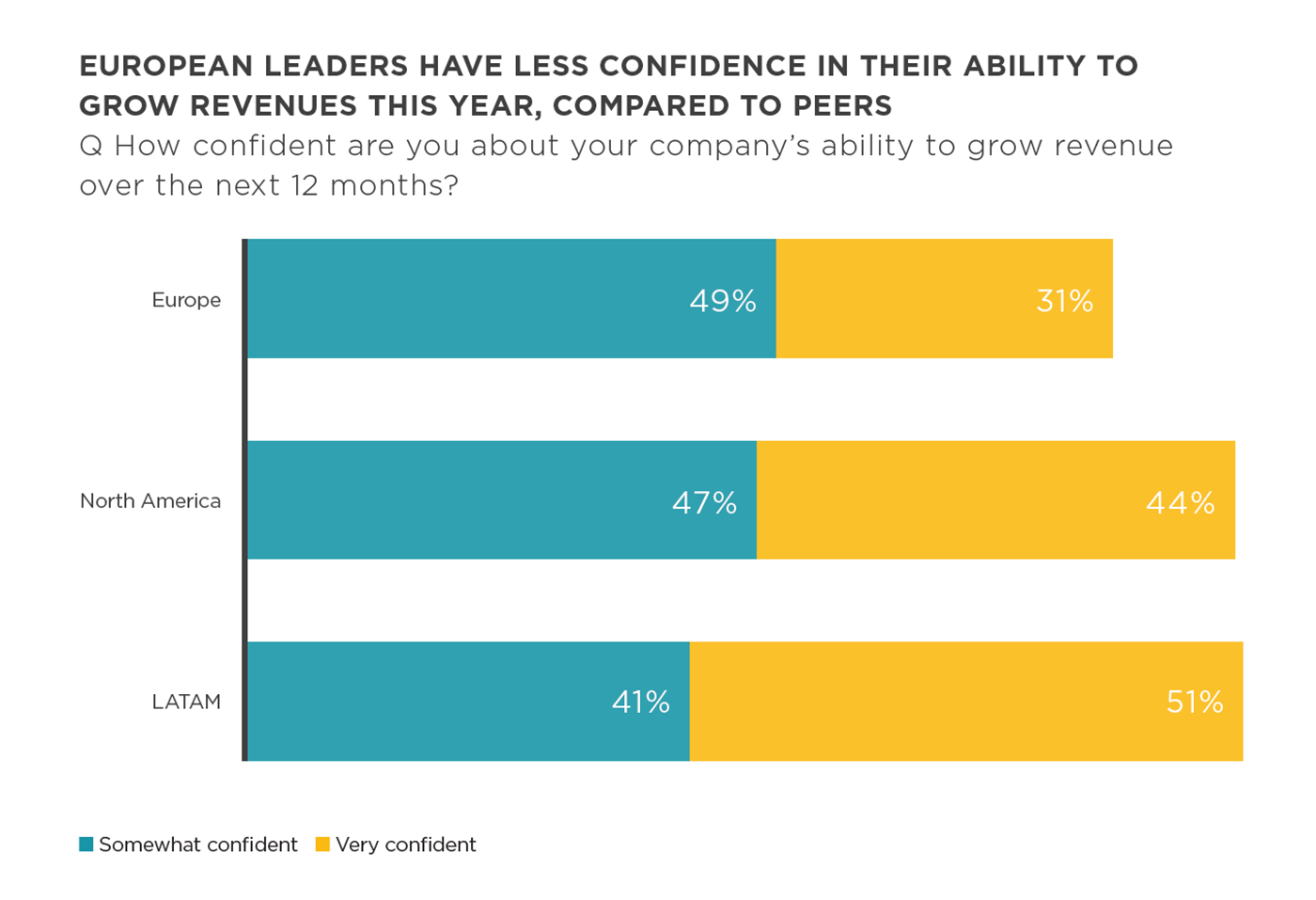

Quizás tranquilizados por los primeros signos de recuperación, el 80% de los líderes europeos expresan confianza en la capacidad de su empresa para aumentar los ingresos este año. Aunque su sentimiento es mucho más moderado, en comparación con sus pares de América del Norte (91%) o LATAM (92%).

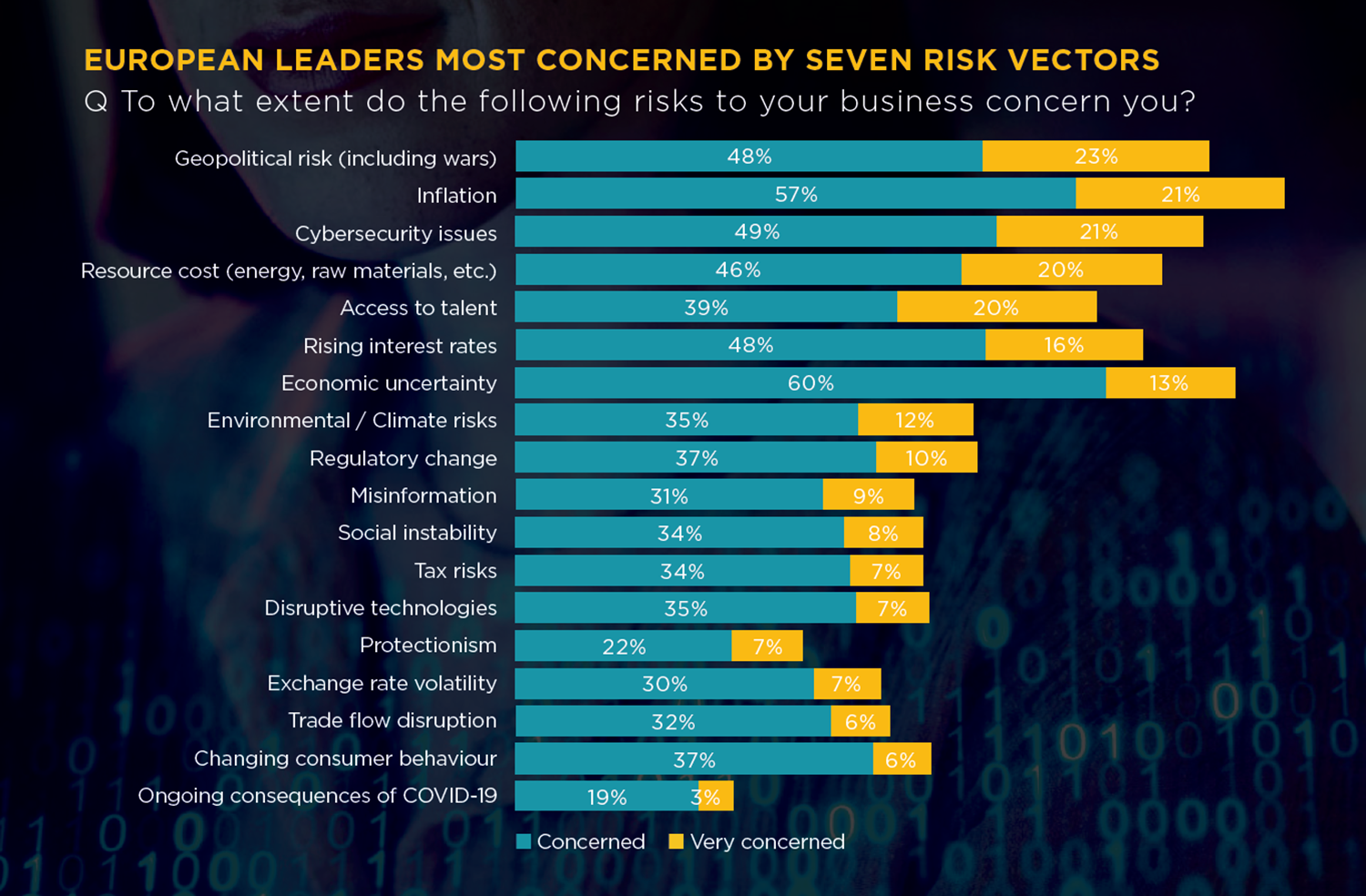

La confianza seguramente se verá afectada por las policrisis incesantes y superpuestas que siguen afectando a los líderes de Europa. Las tres principales preocupaciones de este año son la inflación (78%),

la incertidumbre económica (73%) y los riesgos geopolíticos, incluida la guerra en Europa y Medio Oriente (71%).

Aunque los niveles de preocupación por cada uno de ellos se han reducido sustancialmente en comparación con el año pasado.

La inflación se ha ido desacelerando constantemente. En el segundo semestre de este año,

se espera que el Banco Central Europeo y el Banco de Inglaterra comiencen a reducir gradualmente las tasas de interés. Combinados

con un crecimiento de los salarios reales y un mercado laboral ajustado, estos factores deberían conducir a

un crecimiento regional moderado en 2024.

En general, el radar de riesgo está más concentrado en Europa. Mientras que más de la mitad de los líderes mundiales se sienten

estresados por los impactos de al menos doce factores de riesgo diferentes, la atención de los europeos se centra en siete factores estresantes: económicos (inflación, tasas de interés, incertidumbre del mercado y costos de los recursos), políticos (conflictos en curso), operativos (acceso al talento) y relacionados con la tecnología (ciberseguridad). En comparación con el grupo global, menos líderes están preocupados por los riesgos climáticos

(47% frente a 52%) o el cambio regulatorio (47% frente a 51%).

Sin embargo, la miopía en ambas áreas puede resultar problemática. “Comprender y

mitigar los riesgos, particularmente en ciberseguridad, no es un ejercicio único sino un

viaje continuo. Trabajar con socios tecnológicos de confianza que comprendan la tecnología, aprecien los

beneficios y riesgos comerciales y ayuden a gestionar ambos es fundamental”, señala Mark Butler, socio director de HLB Irlanda.

Los precios competitivos de la energía siguen siendo una preocupación política en Europa, pero también lo es el avance hacia la energía neta cero. El Mecanismo de Ajuste de Carbono en Frontera (CBAM) de la UE entró en vigor en octubre de 2023 y exige nuevas divulgaciones sobre las emisiones de carbono generadas en la producción de ciertos bienes importados a la UE. La Directiva sobre informes de sostenibilidad corporativa (CRSD) de la UE también comenzará a entrar en vigor para las empresas más grandes en el año fiscal 2024.

En 2024, la UE planea reducir aún más el número de permisos de CO2, que permiten a las empresas emitir un determinado volumen de gases de efecto invernadero. Todos estos cambios pueden tener impactos sustanciales en las operaciones comerciales.

Áreas de enfoque clave: personas, procesos y tecnología

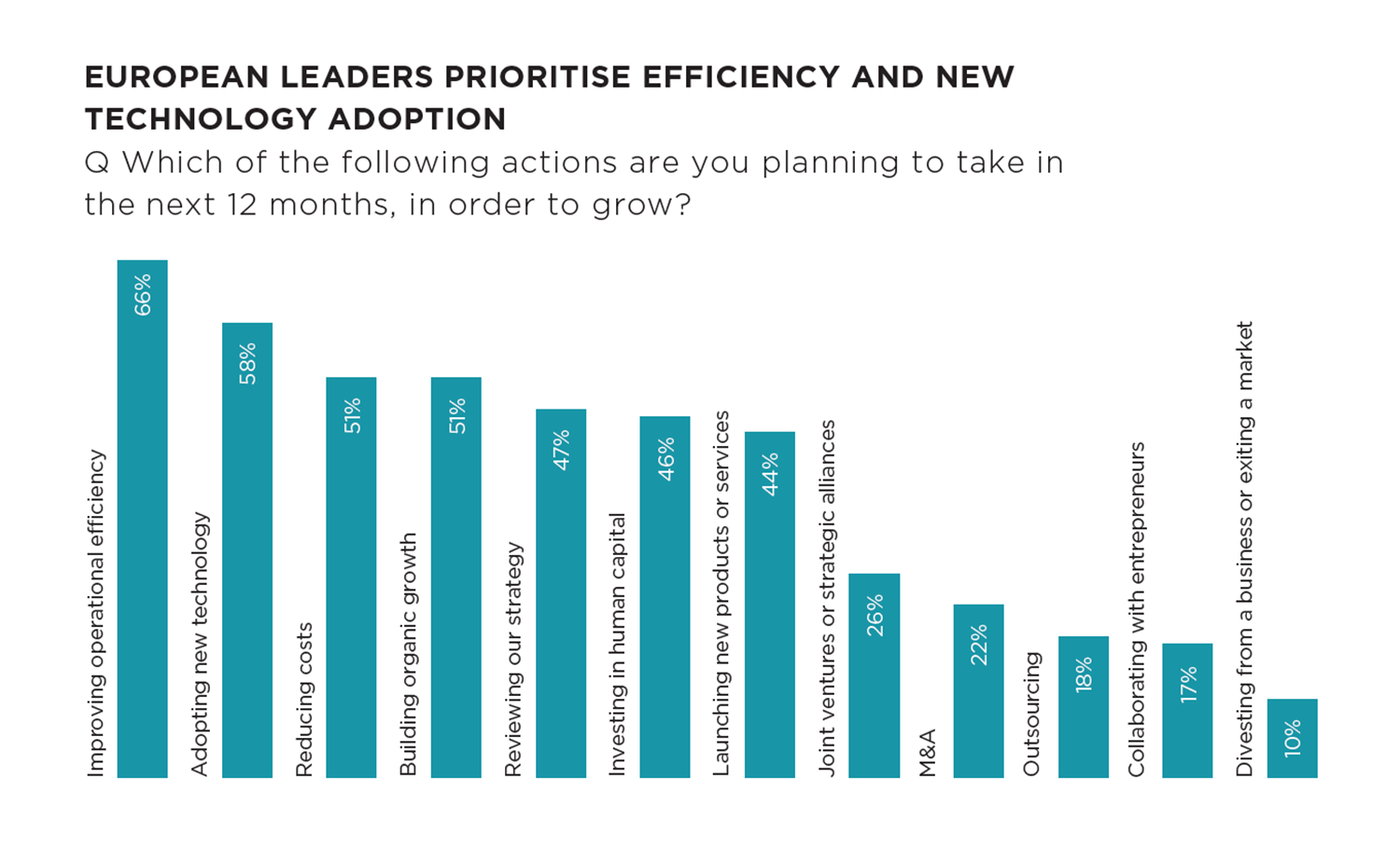

Dados los desafíos actuales, los líderes europeos están enfocados en futuras mejoras comerciales: mejorar la eficiencia operativa (66%) y la adopción de nuevas tecnologías (58%).

La reducción de costes y la creación de un mayor crecimiento orgánico son la tercera prioridad conjunta para el 51%. Este año, el 47% planea revisar su estrategia para lograr crecimiento, en comparación con solo el 35% en 2022.

Sin embargo, el desarrollo de nuevos productos parece menos una prioridad. Solo el 44% planea lanzar nuevos productos o servicios este año frente al 53% en 2022.

En comparación con el comienzo de la década, los líderes europeos están casi dos veces más comprometidos con el uso de las tecnologías como palanca para el crecimiento. Además, están diez puntos porcentuales más inclinados a invertir en capital humano que en 2021. Europa tiene una larga historia de innovación en ingeniería, investigación biomédica y telecomunicaciones.

Sin embargo, ha habido una creciente brecha "digital" entre Europa, América del Norte y China. Desde principios de esta década, tanto Estados Unidos como China han aumentado sustancialmente las inversiones en I+D en tecnología, especialmente en el sector de hardware. En Europa, por el contrario, los niveles de inversión en I+D han ido disminuyendo durante los últimos 15 años.

La I+D en el sector tecnológico recibe cinco veces menos financiación en la Unión Europea que en Estados Unidos. Aunque Europa y el Reino Unido tienen un segmento de empresas tecnológicas de alto rendimiento y

startups unicornio (valoradas en más de mil millones de euros/£), el sector es más modesto en comparación con Estados Unidos o China.

Riesgos que vale la pena asumir: adopción de la IA

Los líderes empresariales en Europa son más conservadores respecto del entorno empresarial internacional que sus pares globales. Saben que la competitividad a largo plazo implica adoptar tecnologías emergentes y mantener una mentalidad "digital".

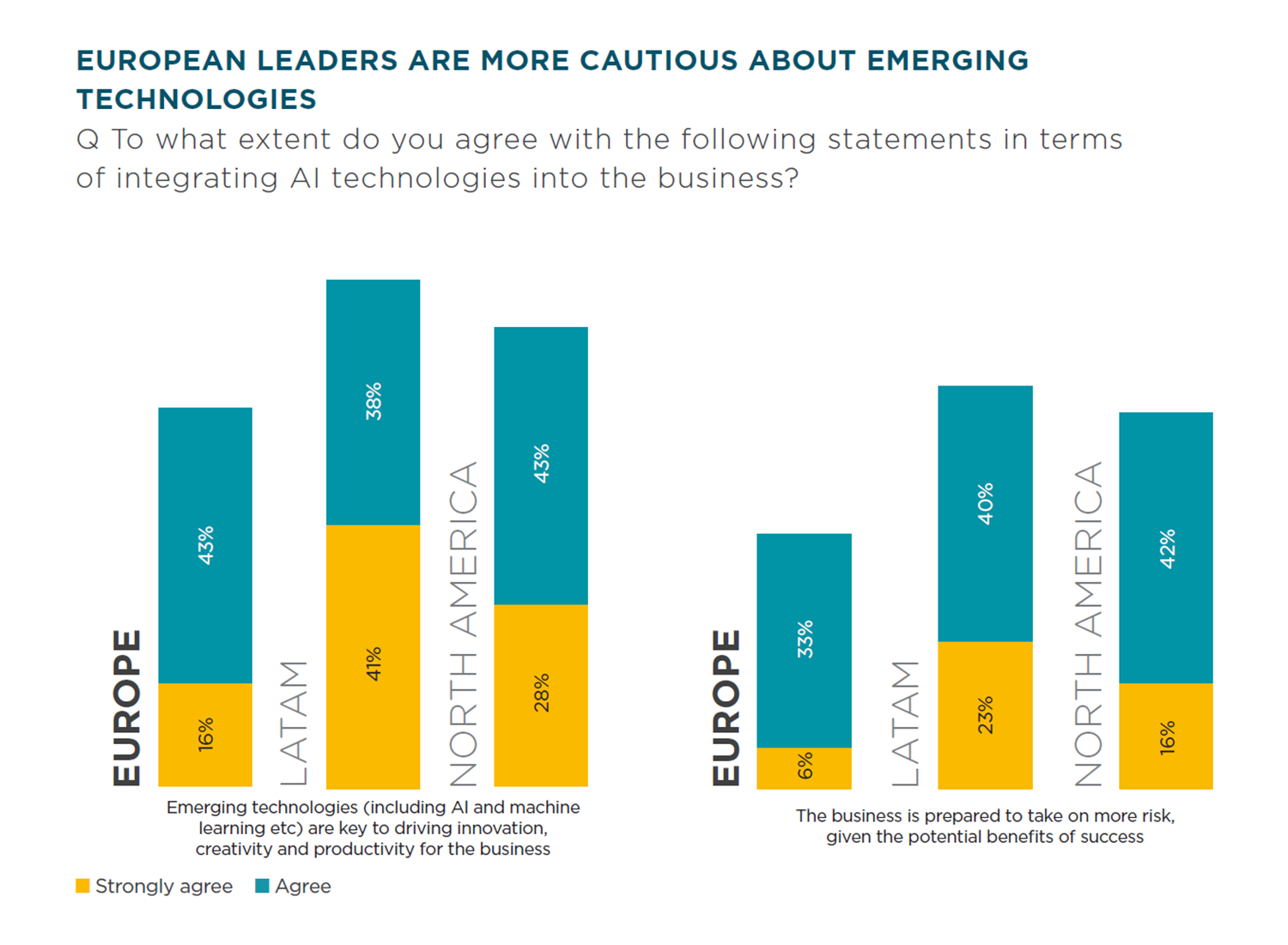

Sin embargo, también son cautelosos a la hora de emprender transformaciones ambiciosas. Aunque el 59% está de acuerdo en que las tecnologías emergentes son clave para impulsar la innovación, la creatividad y la productividad del negocio, sólo el 39% está preparado para asumir más riesgos en esta área, dados los beneficios potenciales del éxito. En comparación, los líderes de América del Norte y LATAM están mucho más dispuestos a aceptar tanto los riesgos como las ganancias que las nuevas tecnologías podrían generar para sus negocios.

La perturbación del comercio también ha sido constante, pero solo la mitad está de acuerdo en que los avances tecnológicos ayudarán a superar futuros desafíos transfronterizos, frente al 63% a nivel mundial. Curiosamente, sin embargo, es menos probable que los líderes europeos mencionen las prioridades de corto plazo y las perturbaciones inesperadas del mercado como barreras para las nuevas inversiones en tecnología, en comparación con sus pares del hemisferio occidental.

Las empresas europeas no parecen tener la IA como una prioridad inmediata. En cambio, están más centrados en la optimización de costos, la gestión de la fuerza laboral y las preocupaciones (geo)políticas inmediatas. La “Ley de IA de la UE”, propuesta en junio de 2023 y que deberá aprobarse en votación final en marzo de 2024, también puede disuadir a algunos líderes de tomar medidas inmediatas.

Las históricas 'leyes de IA' tienen un buen grupo de críticos y partidarios. En el lado positivo, la Ley de IA tiene como objetivo proporcionar un marco legal compartido para desarrollar aplicaciones éticas de IA, protegiendo los derechos y los datos de los usuarios, junto con una infraestructura financiada por la UE para respaldar proyectos de IA. También apunta a facilitar la colaboración en proyectos de IA entre el gobierno, empresas privadas e instituciones de investigación del bloque.

En el lado negativo, la Ley de IA ha sido criticada por su amplia supervisión por parte de los organismos gubernamentales, lo que puede obstaculizar la velocidad de la innovación y la competitividad global de las empresas con sede en la UE. La complejidad de implementar ciertos requisitos también puede disuadir a nuevos participantes en el mercado y retrasar el tiempo de comercialización de nuevos productos, el tipo de acción que los líderes de IA priorizan.

A nivel mundial, las empresas que se identifican como innovadoras en IA tienen 1,3 veces más confianza en su capacidad para aumentar los ingresos este año en comparación con sus pares. También son más propensos a lanzar nuevos productos (56%) este año, buscar alianzas estratégicas con otras empresas y colaborar con emprendedores (32% frente a 13%) para hacer crecer su negocio.

Los líderes europeos se encuentran en la "fase de aprendizaje" de su viaje hacia la IA

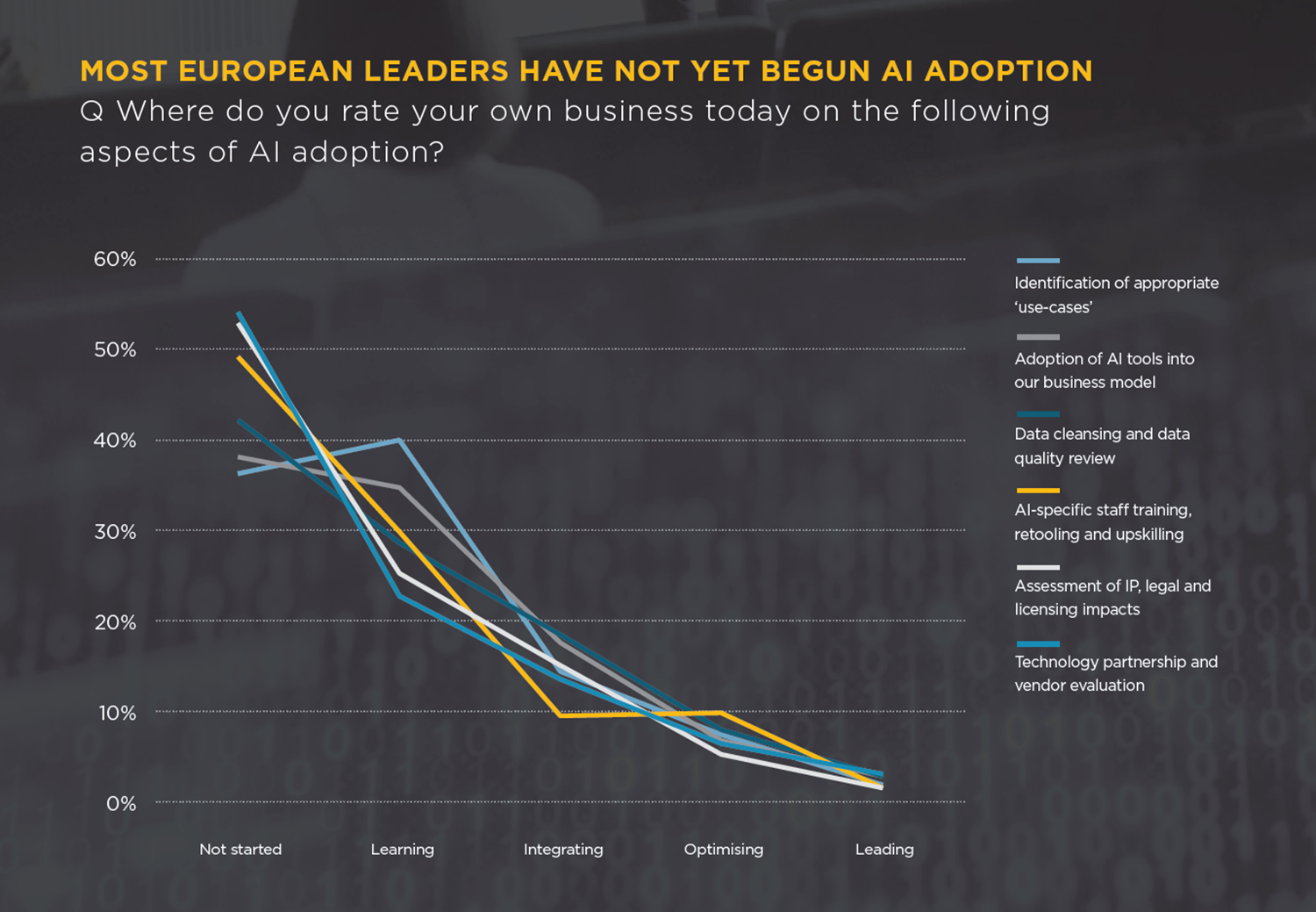

Los líderes europeos todavía están al comienzo de su viaje de adopción: el 30% aún no ha comenzado con la adopción (frente al 21% a nivel mundial), el 45% está conociendo las oportunidades (frente al 37% a nivel mundial), el 15% está integrando la IA en sus operaciones. , mientras que el 8% está optimizando y liderando en este ámbito.

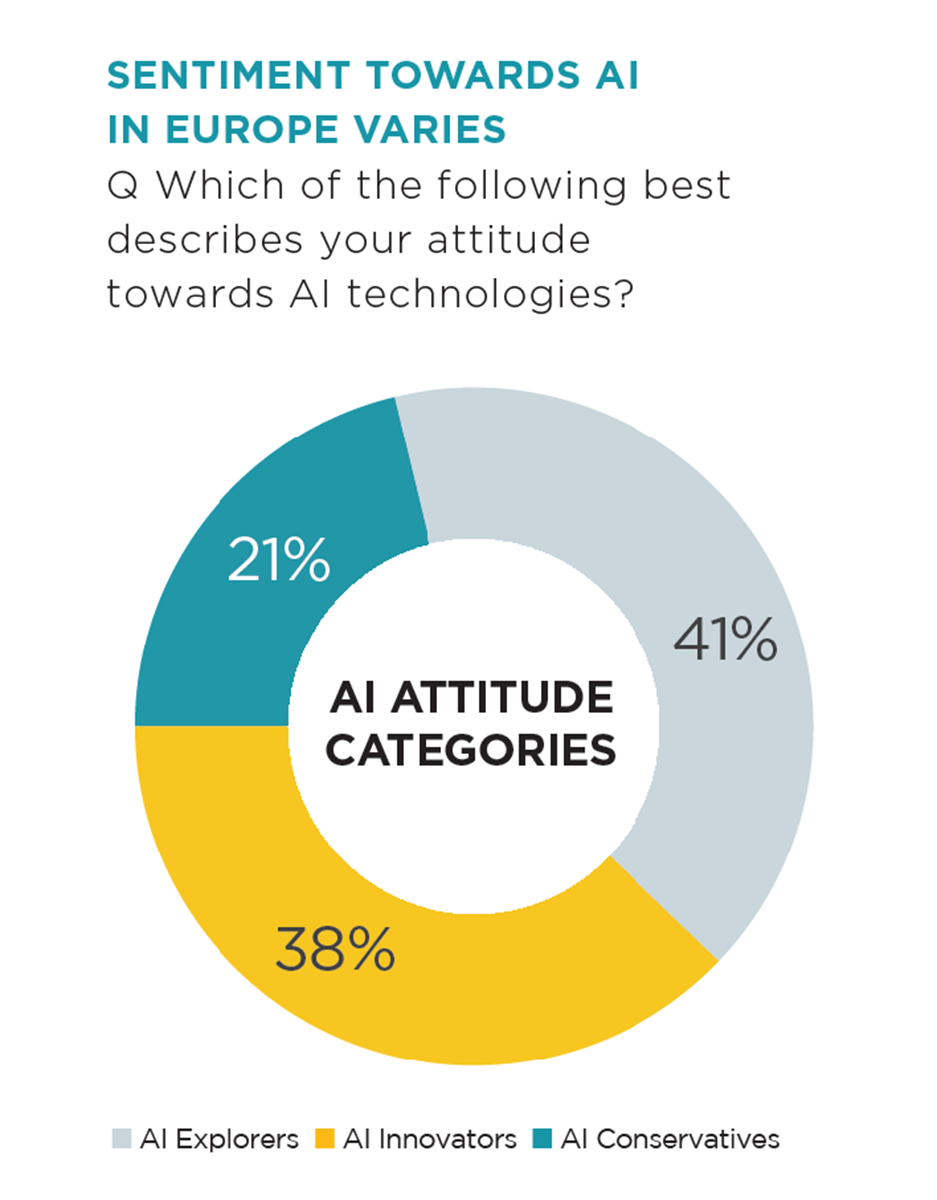

La mayoría de los líderes europeos (41%) se identifican como exploradores. Están dispuestos a implementar tecnologías de inteligencia artificial si existe un argumento comercial convincente para ellos. Otro 38% son innovadores, que ya están utilizando la IA hasta cierto punto o están preparando con entusiasmo un caso de negocio para su adopción. En comparación con todas las regiones, Europa también tiene la mayor fracción de conservadores en IA. El 21% de los líderes europeos se muestran cautelosos o incluso reacios al uso de la IA.

Los líderes europeos han logrado los mayores avances en las tareas básicas para la adopción de la IA: el 29 % ha completado la limpieza de datos y las revisiones de calidad, el 26 % realizó evaluaciones de preparación tecnológica, el 23 % identificó casos de uso de IA apropiados y el 22 % realizó evaluaciones de propiedad intelectual, legales y Impactos de las licencias.

Sin embargo, fundamentalmente los europeos están por detrás de sus pares en la curva de madurez de la IA. En Asia Pacífico, por ejemplo, más del 40% de las empresas afirman que ya están adoptando herramientas de IA en su modelo de negocio, frente a sólo el 28% de los europeos. De manera similar, los líderes norteamericanos lograron el doble de progreso con respecto a la "identificación de casos de uso" y las evaluaciones de las implicaciones regulatorias.

Menos empresas europeas también han completado evaluaciones de proveedores o han iniciado asociaciones tecnológicas que en América del Norte, LATAM, África y Medio Oriente. Un director ejecutivo europeo del sector inmobiliario expresó lo que parece ser el sentimiento general sobre la IA en la región: "Necesitamos dedicar tiempo a aprender los beneficios de la IA y cómo integrarla en nuestras actividades".

El 39% mencionó la "falta de casos de uso y un retorno de la inversión poco claro" como la principal barrera para la adopción. Casi inmediatamente seguido por las preocupaciones sobre la seguridad y privacidad de los datos (38%), siendo la falta de tiempo (35%) la tercera preocupación principal. Sin embargo, la "falta de presupuesto" y el "bajo compromiso ejecutivo" son un problema menor.

Los líderes de varias empresas europeas que cotizan en bolsa también mencionaron la “falta de las habilidades humanas adecuadas para la transformación digital” y la “educación y la conciencia de las oportunidades” como limitaciones actuales. Las pequeñas y medianas empresas (PYMES), a su vez, están buscando un mayor apoyo para formalizar sus argumentos comerciales para la adopción. Los líderes de las PYMES buscan “ilustraciones claras de cómo funciona la IA y los beneficios que la tecnología puede brindar”, “apoyo educativo y de ciberseguridad” y orientación más general sobre las soluciones comerciales disponibles.

Como señala un director ejecutivo del sector minorista: "Todas las empresas enfrentan desafíos que podrían resolverse con una simple integración con una herramienta de inteligencia artificial de terceros, pero simplemente no son conscientes de esa posibilidad". Los líderes europeos parecen tener la mayoría de los recursos internos para lograr transformaciones en IA. Sin embargo, se muestran reacios a lanzarse de lleno al proyecto.

Es una buena práctica cierta cautela, ya que las implicaciones de la nueva tecnología sólo parecen obvias en retrospectiva. Sin embargo, “demasiadas de las preocupaciones destacadas podrían ralentizar la adopción”, señaló un director de operaciones de un sector tecnológico.

Es más probable que los líderes europeos exploren sus opciones

La mayoría de los líderes europeos (41%) se identifican como exploradores. Están dispuestos a implementar tecnologías de inteligencia artificial si existe un argumento comercial convincente para ellos. Otro 38% son innovadores, que ya están utilizando la IA hasta cierto punto o están preparando con entusiasmo un caso de negocio para su adopción.

En comparación con todas las regiones, Europa también tiene la mayor fracción de conservadores en IA. El 19% de los líderes europeos se muestran cautelosos o incluso reacios al uso de la IA.

Los innovadores en IA parecen estar avanzando para conseguir una mejor posición al inicio del nuevo ciclo de crecimiento, mientras que los conservadores en IA parecen estar preparándose para otra recesión económica. Contraintuitivamente, los innovadores en IA están más preocupados por el clima geopolítico, la inflación y los riesgos de ciberseguridad que los exploradores y conservadores de la IA.

La mitad de los innovadores europeos en IA planean lanzar nuevos productos este año. Los conservadores de la IA, a su vez, están mayormente comprometidos con la reducción de costos (49%) y buscan mejoras en la eficiencia operativa (47%).